Retirement Basics

Retirement planning is about more than reaching a number—it's about building flexibility, dignity, and long-term confidence. At V & V Advisors, we focus on simple, evidence-backed strategies families can rely on throughout their lifetime.

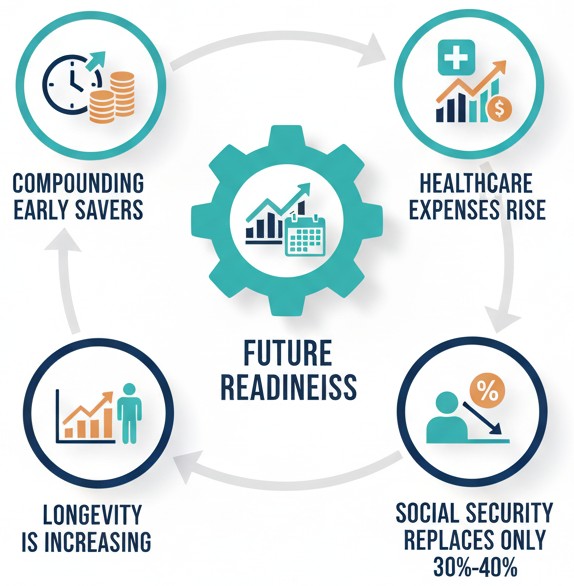

Why Retirement Planning Matters

Whether retirement is 5 or 40 years away, your future depends on decisions you make today. Research from the U.S. Department of Labor (DOL) shows that Americans risk falling short in retirement not because they didn’t save—but because they started too late.

- Compounding rewards early savers — even small amounts grow significantly over time.

- Healthcare expenses rise with age—retirees often spend $4,000–$7,000/year out-of-pocket.

- Social Security replaces only 30%–40% of most workers’ income.

- Longevity is increasing—meaning your savings must last longer.

Sources: DOL; Social Security Administration; Fidelity Retiree Health Index

The Power of Compounding

Compounding means your interest earns interest. The earlier you start, the easier retirement becomes. These estimates are based on Investor.gov’s compound interest calculator.

| Starting Age | Monthly Savings | Years of Growth | Value at 65 (7% growth) |

|---|---|---|---|

| 25 | $200 | 40 years | ≈ $479,000 |

| 35 | $200 | 30 years | ≈ $245,000 |

| 45 | $200 | 20 years | ≈ $98,000 |

*Estimates based on historical average market performance; actual results vary.

Key Building Blocks of Retirement Planning

1. Employer-Sponsored Plans (401(k), 403(b), 457)

These accounts allow you to contribute pre-tax money, lowering your taxable income. Always aim to capture the full employer match—it’s essentially a guaranteed return.

Source: DOL – Saving Matters Program

2. IRAs (Traditional & Roth)

IRAs offer tax-advantages to help your savings grow. Roth IRAs grow tax-free; Traditional IRAs offer tax deductions. Contribution limits and income rules apply.

Source: IRS – Retirement Plan FAQs

3. Asset Allocation

Diversifying between stocks, bonds, and cash helps manage risk. Younger savers typically lean more toward equities; older savers shift toward stability.

4. Social Security

Most retirees rely on Social Security, but it’s not intended to be the full plan. You can estimate your benefits at: SSA.gov/myaccount.

5. Emergency Funds & Insurance

Even strong retirement plans can unravel without protection. Ensure emergency savings, disability insurance, and life insurance are in place.

6. Tax Strategy

Combining pre-tax, Roth, and taxable accounts can give you flexibility in retirement. Tax diversification helps manage withdrawals and reduce tax costs.

A Simple Retirement Timeline

- 20s–30s: Start early, contribute consistently, capture employer matches.

- 40s: Increase contributions, reduce high-interest debt, protect income.

- 50s: Catch-up contributions begin at age 50; reassess investment mix.

- 60s: Plan Social Security timing, calculate withdrawal needs, prepare for Medicare.

- 65+: Manage income sources, protect against market downturns, simplify finances.

Source: CFPB – Retirement Management Guide

Retirement Readiness Checklist

- You know your retirement age and income goal.

- You contribute regularly to retirement accounts.

- You review your investments at least annually.

- Your emergency fund covers 3–6 months of expenses.

- You have a plan for healthcare and Medicare.

- You understand how long-term care may impact your future.

- You’re aware of Social Security benefit options.

Build Your Confident Retirement Plan

At V & V Advisors, we believe retirement planning should feel empowering—not overwhelming. Explore more lessons in our Financial Education Series, or reach out for personalized guidance.

Book Consultation