Budgeting Basics

At V & V Advisors, we view a budget as more than a spreadsheet. It’s a simple plan for how your money supports your family today and your goals for tomorrow. This page walks through what a budget is, why it matters, and how to create one you can actually stick with.

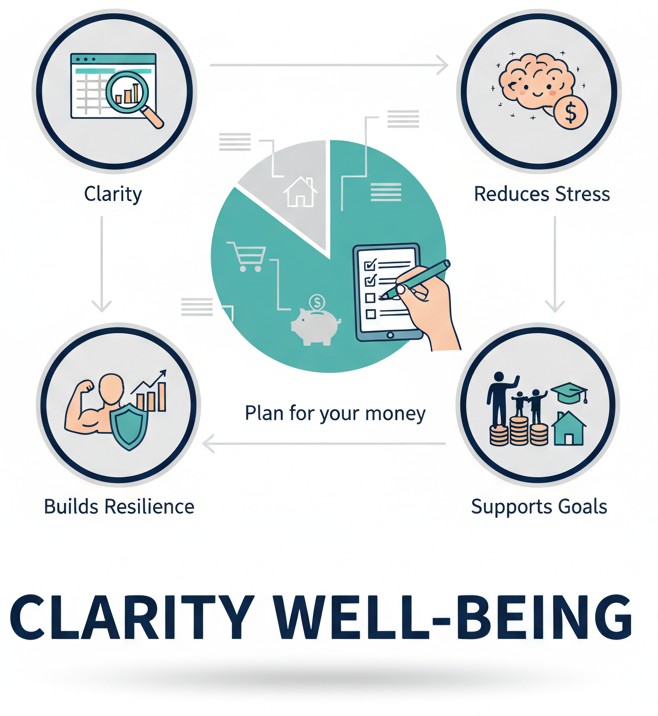

Why Budgeting Matters

A budget is a plan for your money. Instead of wondering where your paycheck went, you decide in advance what matters most – housing, food, savings, debt payoff, and family goals.

- Gives clarity. You see what’s coming in, what’s going out, and where you can adjust.

- Reduces money stress. Having a plan helps you feel more in control when bills or surprises pop up.

- Builds resilience. Research from agencies like the CFPB and nonprofit educators finds that people who track spending and plan ahead are better able to handle financial shocks like job loss, car repairs, or medical bills.

- Supports long-term goals. A budget is how you turn goals like college savings, travel, or paying off a mortgage into monthly, realistic actions.

Sources: CFPB – Budgeting & saving tools , NEFE – Financial well-being research

How to Build Your Budget – Step by Step

You don’t need to be “good with numbers” to build a budget. Start simple and refine over time.

| Step | What to Do |

|---|---|

| 1. Calculate Your Take-Home Income | Add up your reliable monthly income after taxes and payroll deductions (salary, wages, benefits, and any consistent side income). If your income fluctuates, consider using a conservative average based on the last 3–6 months. |

| 2. List Your Essential Expenses | Include housing, utilities, transportation, groceries, insurance premiums, minimum debt payments, and childcare or school costs. These are your “must pay” bills. |

| 3. Add Savings & Debt Paydown | Treat savings like a bill you pay to your future self – emergency fund, retirement, and extra debt payments. Even small, regular amounts matter and build over time. |

| 4. Plan for Non-Essentials (“Wants”) | Now layer in dining out, subscriptions, entertainment, and shopping. The goal isn’t to cut everything, but to be intentional and keep these in line with your priorities. |

| 5. Compare Plan vs. Reality Each Month | At the end of the month, compare what you planned to what actually happened. Look for patterns: where did you overspend, where did you underspend, and what needs to change? |

Understanding Needs vs. Wants

Many families feel stuck not because they don’t earn enough, but because their money isn’t aligned with what matters most. A simple filter:

- Needs: You cannot live or work safely without it (housing, basic food, utilities, transportation to work, essential insurance, minimum loan payments).

- Wants: Nice-to-haves that add comfort or enjoyment (eating out, streaming services, travel upgrades, non-essential shopping).

At V & V Advisors, we often start by protecting the essentials (Needs), then redirecting even a small portion of Wants toward savings and debt reduction.

Popular Budgeting Methods

There is no one “perfect” way to budget. The best method is the one you can follow consistently. Here are three widely used approaches:

50-30-20 Rule

A simple rule of thumb: allocate about 50% of your take-home pay to needs, 30% to wants, and 20% to savings and debt repayment. Many consumer education organizations use this as a starting point for new budgeters.

Zero-Based Budgeting

Every dollar has a job. You plan your income minus expenses (including savings and debt payments) so it equals zero. This doesn’t mean your bank balance is zero — it means every dollar is assigned on purpose before the month begins.

Envelope (or Digital Envelope) System

You divide spending into categories (groceries, gas, dining, etc.) and assign a set amount to each. Traditionally, people used physical envelopes with cash; today many families use banking apps or digital tools to replicate the same “once it’s gone, it’s gone” guardrail.

Examples and educational use of these methods can be found through: CFPB Budgeting tools, NEFE, and other nonprofit financial education resources.

Sample Monthly Budget Snapshot

Below is a simple example for a family with $4,000 in monthly take-home income using a 50-30-20 style split. Your numbers will be different, but the structure is similar.

| Category | Example Amount | Notes |

|---|---|---|

| Needs (~50%) | $2,000 | Rent/mortgage, utilities, groceries, transportation, minimum debt payments, insurance. |

| Wants (~30%) | $1,200 | Dining out, streaming, hobbies, gifts, non-essential shopping, travel. |

| Savings & Debt (~20%) | $800 | Emergency fund contributions, retirement, college savings, extra debt payments. |

This example is for educational purposes only. It is not a recommendation or individualized financial advice. Your allocation should reflect your income, cost of living, obligations, and goals.

Your Next Step

Choose one small action to take this week:

- List your last 30 days of spending from your bank or credit card app.

- Estimate your monthly take-home income and essential expenses.

- Pick one method (50-30-20, zero-based, or envelopes) to try next month.

You can use our Budget Worksheet or any app/spreadsheet you prefer. The goal is progress, not perfection.

Budget Worksheet (Excel)

At V & V Advisors, budgeting is part of your broader financial foundation: earning, spending, protecting, and investing with intention. As your protection and planning conversations deepen (insurance, college planning, retirement, and more), this basic budget becomes the framework we build on together.