Emergency Funds

An emergency fund is the foundation of financial stability — a safety net that protects your family from unexpected challenges without turning to debt.

What Is an Emergency Fund?

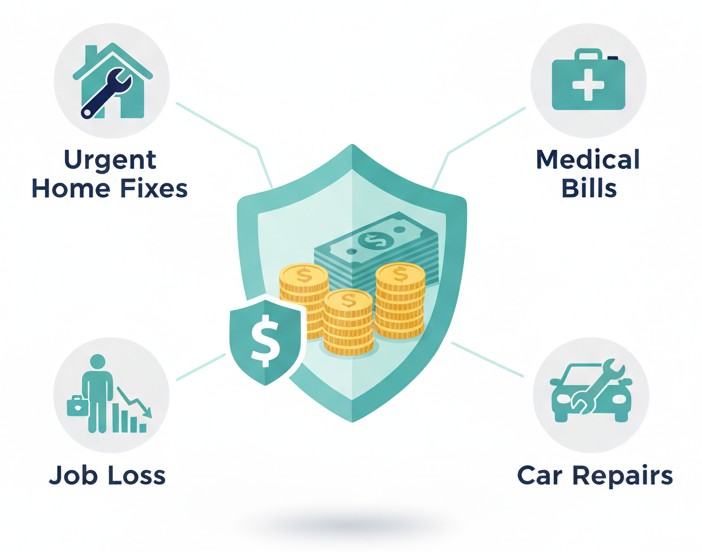

An emergency fund is money set aside for unplanned expenses such as medical bills, job loss, car repairs, or urgent home fixes. It helps you stay financially stable without relying on high-interest credit cards or loans.

Research from the Consumer Financial Protection Bureau (CFPB) shows that households with even a small emergency cushion experience significantly less financial stress during unexpected events.

Source: CFPB – Building Your Savings

Why Emergency Funds Matter

Emergencies are part of life — but financial crises don’t have to be. Without savings, even small setbacks can lead to missed bills, mounting interest, or increased stress. With savings, families gain freedom and flexibility.

- Reduces reliance on credit during emergencies

- Helps prevent long-term financial setbacks

- Supports mental and emotional well-being

- Creates stability during job loss or medical events

The National Endowment for Financial Education (NEFE) reports that 67% of Americans experienced an unexpected financial shock in the last year — and most were unprepared.

Source: NEFE – Saving for Emergencies

How Much Should You Save?

Start with a simple, achievable milestone: $500–$1,000 for immediate emergencies such as car repairs or medical co-pays. Over time, aim for:

- 3 months of expenses — stable income

- 6 months — dependents or variable income

- 9–12 months — self-employed households

Source: CFPB & Federal Reserve – Economic Well-Being Report

Where Should You Keep It?

A good emergency fund must be:

- Safe — FDIC-insured account

- Accessible — available within 24–48 hours

- Separate — not mixed with daily spending money

The best choices are:

- High-yield savings account

- Money market account

- Short-term treasury-backed savings

How to Build Your Fund

1. Automate weekly or payday transfers

2. Save windfalls: bonuses, refunds, small tax credits

3. Cut one small expense temporarily (coffee, dining out)

4. Use the “round-up” feature on banking apps

5. Sell unused items or redirect side-income

Source: Pew Research – Household Financial Security Report

What Counts as a True Emergency?

Not every unexpected expense should come from the emergency fund. Use it only for essential, urgent situations:

| Appropriate Use | Not an Emergency |

|---|---|

| Job loss or reduced income | Vacations, sales, or entertainment |

| Major medical or dental expenses | Holiday shopping or gifts |

| Urgent car or home repairs | Upgrades or optional purchases |

| Unexpected family emergencies | Everyday budget shortfalls |

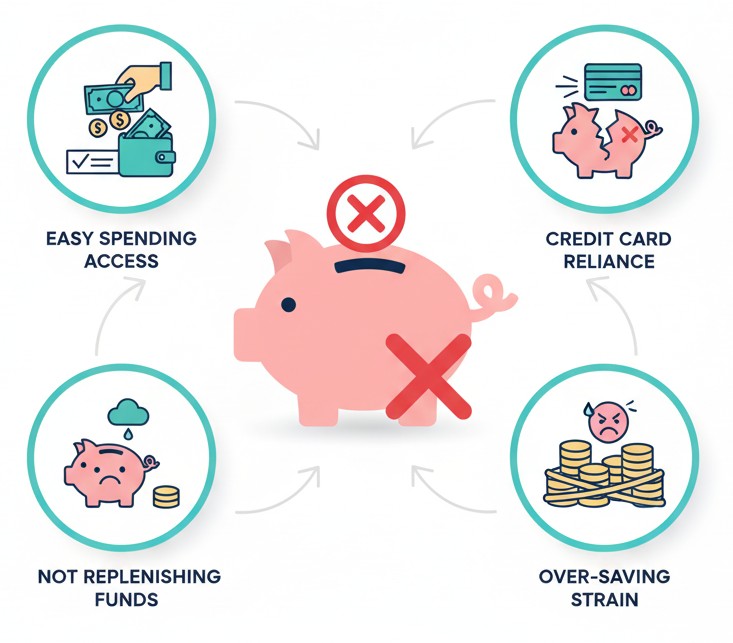

Common Mistakes to Avoid

- Keeping emergency savings in checking where it’s easy to spend

- Using credit cards as an alternative to savings

- Not replenishing the fund after an emergency

- Saving too aggressively and causing cash-flow strain

Take Your First Step Today

You don’t need thousands of dollars to begin. What matters most is consistency. Even $10–$25 per week builds momentum. Over time, your emergency fund becomes the bedrock of your financial confidence.

At V & V Advisors, we help families build strong financial habits that support protection, resilience, and long-term wealth.