Managing Debt

Debt can support major life goals—or create long-term stress. At V & V Advisors, we teach families how to manage debt intentionally, reduce high-interest burdens, and build a foundation for financial peace and stability.

Understanding Good vs. Bad Debt

Not all debt is harmful. Some debt helps you build long-term value, while other debt drains your income through high interest. Understanding the difference helps you set clear priorities.

- Good Debt: Mortgages, student loans, and business loans that support long-term growth.

- Bad Debt: High-interest credit cards, payday loans, and consumer financing with 20–30% APR.

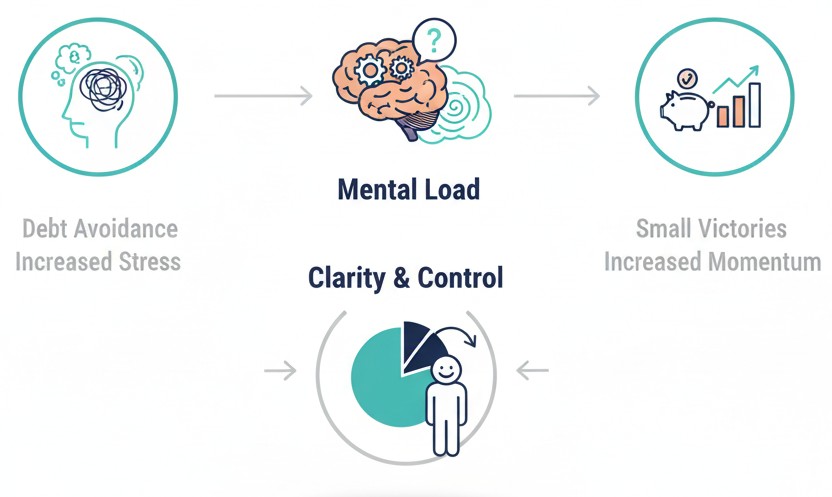

The Psychology of Debt

Research from the Federal Reserve shows that debt creates mental load, decision fatigue, and avoidance behaviors. This is why small, early wins (like the Debt Snowball method) are often more motivating—even if they aren’t mathematically optimal.

- Debt avoidance increases stress and reduces planning capability.

- Small victories increase momentum and confidence.

- Clarity reduces anxiety and supports healthier financial choices.

Source: Federal Reserve – Consumer & Community Research

Building a Debt Repayment Plan

A great plan is not the “perfect” method—it’s the one you can stick with consistently. These two approaches are recommended by financial education organizations:

- Debt Snowball: Pay off the smallest balance first to build momentum.

- Debt Avalanche: Pay off the highest interest rate first to save the most money.

Pro Tip: Automate payments. Most late fees and credit score drops happen due to missed payments, not inability to pay.

How Interest Really Works

Many families underestimate how interest compounds against them. High-interest cards (20–29% APR) can double the cost of a purchase if only minimum payments are made.

| Balance | APR | Minimum Payment | Time to Pay Off |

|---|---|---|---|

| $3,000 | 22% | $70 | ~8.5 years |

| $10,000 | 25% | $250 | ~11 years |

Source: Federal Reserve – Credit Card Interest Simulation Tools

Managing Credit Cards Wisely

Credit cards are powerful, but only when used intentionally. Carrying a balance triggers high interest and reduces credit score health.

- Keep utilization below 30% (CFPB guideline).

- Aim to pay the full balance each month.

- Never miss a due date—set reminders or auto-pay.

Check your credit reports yearly at AnnualCreditReport.com.

Source: FDIC – Responsible Credit Use

Debt Prioritization Matrix

Use this simple framework to know where to focus first.

| Debt Type | Typical APR | Priority Level |

|---|---|---|

| Payday Loans | 200–400% | Urgent |

| Credit Cards | 18–29% | High |

| Personal Loans | 8–20% | Medium |

| Student Loans | 4–7% | Lower |

| Mortgage | 3–6% | Long-term |

Source: CFPB & Federal Reserve APR Trends

When You Feel Overwhelmed

If your debt feels unmanageable, nonprofit credit counselors can provide genuine help—not sales pitches.

Staying Debt-Free

Once you’ve reduced your debt, protect your progress with clear routines:

- Build a 3–6 month emergency fund

- Track spending monthly

- Avoid impulse purchases or financing offers

- Review credit every 4 months (rotating bureaus)

Financial freedom is not a single moment—it’s a lifelong habit built on consistent choices.