How Life Insurance Fits Into a Financial Plan

Life insurance isn’t just about protecting against loss — it’s about strengthening your entire financial plan. When done thoughtfully, it safeguards income, supports long-term goals, and creates generational stability.

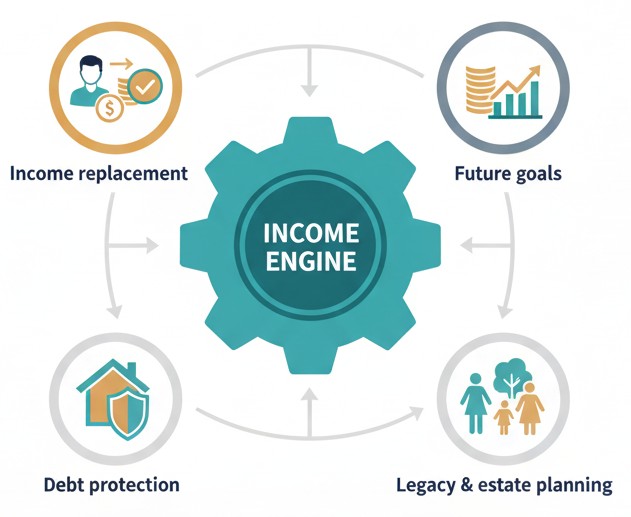

Why Life Insurance Matters in a Financial Plan

According to the CFPB and Federal Reserve, a family’s income is the engine that makes budgeting, saving, investing, and debt reduction possible. Life insurance protects that engine.

- Income replacement — ensures financial obligations continue

- Debt protection — mortgages, student loans, and family costs

- Future goals — education, retirement, and long-term plans

- Legacy and estate planning — smooth transfer of wealth

Sources: CFPB Household Financial Well-Being Report, Federal Reserve Economic Well-Being Study.

The Household Financial Flow Model

At V & V Advisors, we help families understand how money flows through their life. Life insurance plays a role in stabilizing every part of this flow:

| Financial Area | Household Impact | Life Insurance Role |

|---|---|---|

| Income | Supports bills, lifestyle, savings, and family needs | Replaces lost income to prevent financial collapse |

| Expenses & Debt | Mortgage, childcare, food, transportation | Pays off or reduces burdens for surviving family |

| Savings | Emergency fund, short-term goals | Prevents depletion after a major family event |

| Long-Term Goals | College planning, retirement, wealth building | Ensures goals stay funded even after tragedy |

How Term vs. Permanent Life Insurance Fit Into Planning

Different types of life insurance play different roles inside a financial plan. Here’s how they support families at various stages:

| Type | Best For | Financial Planning Role |

|---|---|---|

| Term Life Insurance | Income earners, young families, mortgage protection | Low-cost, high coverage for income replacement and major obligations |

| Whole Life Insurance | Long-term stability, legacy, estate needs | Guaranteed protection + cash value for lifetime planning |

| Universal Life (UL) | Flexible, adjustable coverage | Long-term coverage that adapts to changing financial needs |

| Indexed Universal Life (IUL) | Growth-oriented planning, long-term protection | Potential for market-linked growth with downside protection |

| Final Expense / GIWL | Seniors, families needing guaranteed approval | Ensures no financial burden for end-of-life costs |

Where Cash Value Can Add Planning Advantages

While not needed for everyone, cash value life insurance can be a long-term planning tool when used responsibly and aligned with goals. Research from the Insurance Information Institute shows it can support:

- Supplemental retirement income (policy-dependent)

- Tax-advantaged accumulation

- Access to funds during emergencies

- Guaranteed growth (whole life)

Source: Insurance Information Institute (III).

Life Insurance Across Life Stages

Life insurance needs evolve as your life changes. Here’s how it fits into common life stages:

| Life Stage | Primary Focus | Planning Fit |

|---|---|---|

| Young Adults | Low-cost protection, start early for lower premiums | Term life for income protection |

| Growing Families | Mortgage, childcare, debts | High term coverage + strategic permanent if needed |

| Mid-Life | Retirement planning & wealth building | UL/IUL or whole life for stability + long-term goals |

| Seniors | Legacy, final expenses, estate transfer | Whole life or guaranteed issue |

How Life Insurance Supports Generational Wealth

Life insurance is one of the most efficient tools for transferring wealth tax-efficiently. NAIC notes that beneficiary proceeds generally avoid probate and are delivered quickly to families.

- Helps eliminate debt before passing assets to children

- Creates an instant estate for the next generation

- Provides liquidity for taxes or final expenses

- Keeps family goals (education, business, home) on track

Family Planning Checklist

- Would your family be financially stable if income stopped?

- Do you have the right amount of coverage for your goals?

- Are your beneficiaries updated and structured correctly?

- Do you understand the role of each type of coverage you own?

- Does your protection plan match your life stage?