How to Choose the Right Protection Strategy

A strong protection strategy shields your income, safeguards your family, and keeps your long-term goals on track. The right plan balances risk, affordability, and future needs — not just today’s concerns.

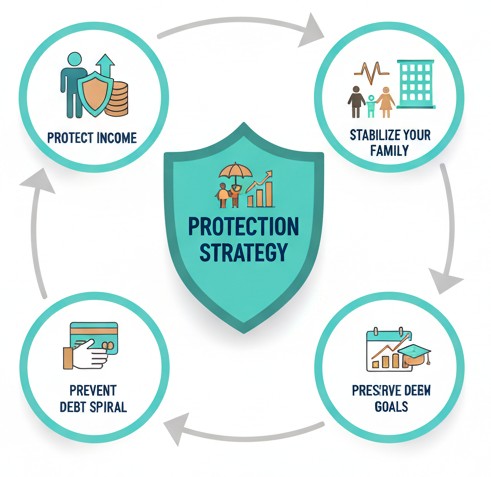

Why Your Protection Strategy Matters

According to the Consumer Financial Protection Bureau (CFPB), unexpected financial shocks — such as income loss, medical events, or property damage — are among the leading causes of long-term financial hardship.

A protection strategy is more than insurance. It’s an intentional approach to:

- Protect income — the foundation of your financial life

- Stabilize your family during medical or life events

- Prevent debt spiral after unexpected emergencies

- Preserve long-term goals such as retirement and college

Source: CFPB – Financial Well-Being Research

The Protection Strategy Pyramid

V & V Advisors teaches a layered approach to protection — starting with the essentials and building upward.

| Layer | Purpose |

|---|---|

| 1. Income Protection | Life insurance & disability benefits to replace lost income. |

| 2. Family Protection | Coverage for dependents, surviving spouse, childcare, debt payoff. |

| 3. Asset Protection | Home, auto, liability, and long-term care protection. |

| 4. Wealth Continuity | Estate planning, trusts, tax-efficient wealth transfer. |

This structure aligns with guidance from the Insurance Information Institute (III) and NAIC on prioritizing essential risks before optional enhancements.

A Step-by-Step Way to Choose the Right Strategy

The best protection strategy is one that matches your goals, risks, and resources. Here’s our framework:

- 1. Assess Your Income — How much income needs to be replaced?

- 2. Identify Family Needs — Dependents, childcare, mortgage, lifestyle.

- 3. Evaluate Health & Risks — Family medical history, chronic conditions, job risk.

- 4. Prioritize Goals — Debt payoff, wealth building, legacy, stability.

- 5. Match Coverage to Needs — Term, whole life, IUL, LTC, riders.

- 6. Review Affordability — A good plan should be sustainable over time.

Based on NAIC Consumer Planning Guidelines.

Matching Your Strategy to Your Life Stage

Protection needs shift as life changes. Here's a clear way to think about it:

| Life Stage | Primary Needs | Key Solutions |

|---|---|---|

| Young Adults | Income protection, debt coverage | Term life, disability riders |

| Growing Families | Replace income, childcare, mortgage | Term life, child rider, living benefits |

| Mid-Career | Long-term planning, early wealth building | Term + permanent blend, IUL/whole life |

| Pre-Retirement | Debt-free transition, LTC concerns | Permanent life, LTC riders |

| Retirement | Legacy, tax-efficient transfer | Permanent life, trust planning |

Protection Strategy Decision Matrix

This matrix helps clarify which type of coverage fits typical goals.

| Goal | Best Fit | Why |

|---|---|---|

| Highest coverage at lowest cost | Term Life | Covers major income years affordably. |

| Lifetime protection | Whole Life / IUL | Permanent coverage for final expenses, legacy, or income planning. |

| Tax-advantaged wealth building | IUL / Whole Life | Cash value can support long-term goals. |

| Long-term care concerns | LTC Rider / Hybrid Policies | Mitigates high medical and care expenses. |

| Estate planning | Permanent Life + Trusts | Coordinates with legal planning to transfer wealth efficiently. |

How V & V Advisors Helps You Build the Right Strategy

Families are often unsure which protection options to choose. Our approach focuses on clarity, education, and long-term fit — not product pushing.

- We help you analyze risks and income dependence.

- We clarify coverage gaps and existing protections.

- We design strategies based on your goals, budget, and timeline.

- We guide you through policy types, riders, and features.

- We focus on sustainability — a plan you can keep long-term.